Strategy

Materiality and stakeholder analysis

Materiality analysis

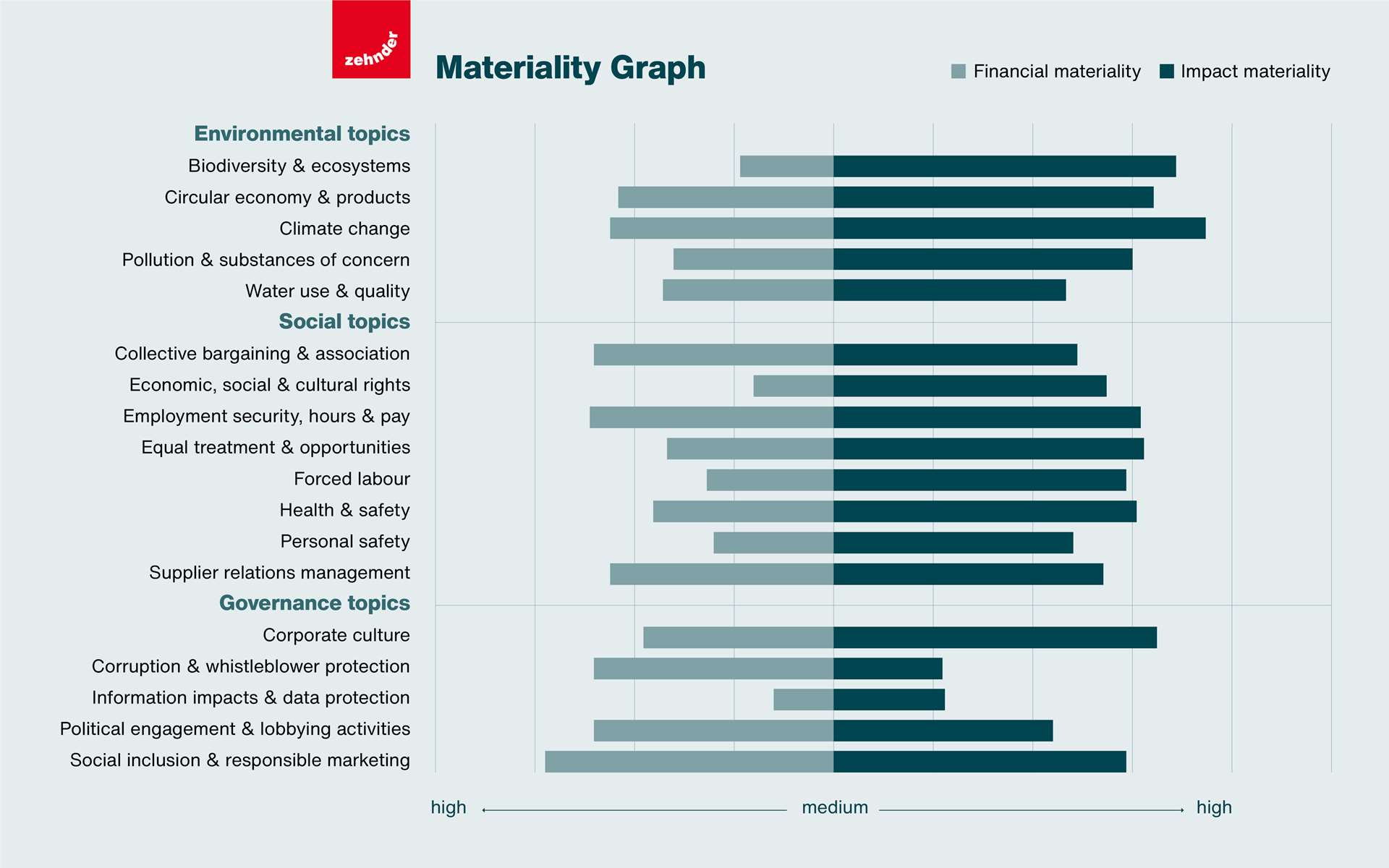

The materiality analysis is our foundation for identifying key issues for both the company itself and its stakeholders. Following the double materiality assessment approach, we focused on topics with a significant impact on people, society and the environment that are relevant to our business.

We review our materiality analysis regularly. In 2023, we updated our materiality assessment process and updated the previous materiality matrix to match the GRI and ESRS guidelines, supported by an external consulting agency. Based on a comprehensive list of sustainability matters provided by ESRS1, Zehnder’s sustainability team drew up a net list of about 80 items relevant to Zehnder Group and its value chain. These were further categorised into 20 topics.

We then conducted 41 interviews with “affected stakeholders” and “users of sustainability statements”. Affected stakeholders are defined by the ESRS as individuals or groups whose interests are currently affected or could be affected by the undertaking’s activities and its direct and indirect business relationships across its value chain. The primary audience for sustainability statements consists of users of general-purpose financial reporting. Additionally, other potential users include governments, analysts and business partners. We analysed our stakeholders accordingly: For affected stakeholders, we interviewed customers, Zehnder employees, end-users of our products, Zehnder Group function heads, Zehnder Group Executive Committee and Board members, suppliers and environmental specialists to act as representatives of the natural world. For users of sustainability statements, we interviewed academics, business partners, government representatives, UNGC representatives, trade union representatives, investors and analysts. Many stakeholders fit into more than one of these categories, but for the purposes of categorisation they were considered to be in the category that we felt best expressed their position relative to Zehnder. In total, we held 34 interviews with affected stakeholders and seven interviews with users of statements. An additional “interview” consisted of the material results of the Human Rights Due Diligence assessment, which was conducted by Zehnder earlier in 2023, making for a total of 42 responses.

The interview partners were presented with the list of 20 topics and asked to identify the top three to five sustainability priorities for Zehnder Group. For each one, insights were identified and categorised as impacts, risks or opportunities and subsequently assessed for materiality, with a specific emphasis on a mid-term perspective spanning five to ten years. If the interviewee had insights into other topics, these were added as well. The assessment included potential and actual effects as well as positive and negative effects. After conducting the interviews, scores for financial materiality and impact materiality were assigned to each topic based on the average results of the insights in that category.

A topic was deemed material if it was significant from a financial or impact perspective or from both perspectives. According to the ESRS, impact materiality is established when a sustainability issue relates to the material actual or potential, positive or negative impacts on people or the environment over the short, medium or long term for the organisation. This includes both direct impact by an organisation’s operations, as well as through its upstream and downstream value chain. Financial materiality is established if a sustainability issue triggers or could reasonably be expected to trigger material financial effects on the organisation. This can include affecting its financial position, financial performance, cash flows, its access to finance or cost of capital over the short, medium or long term.

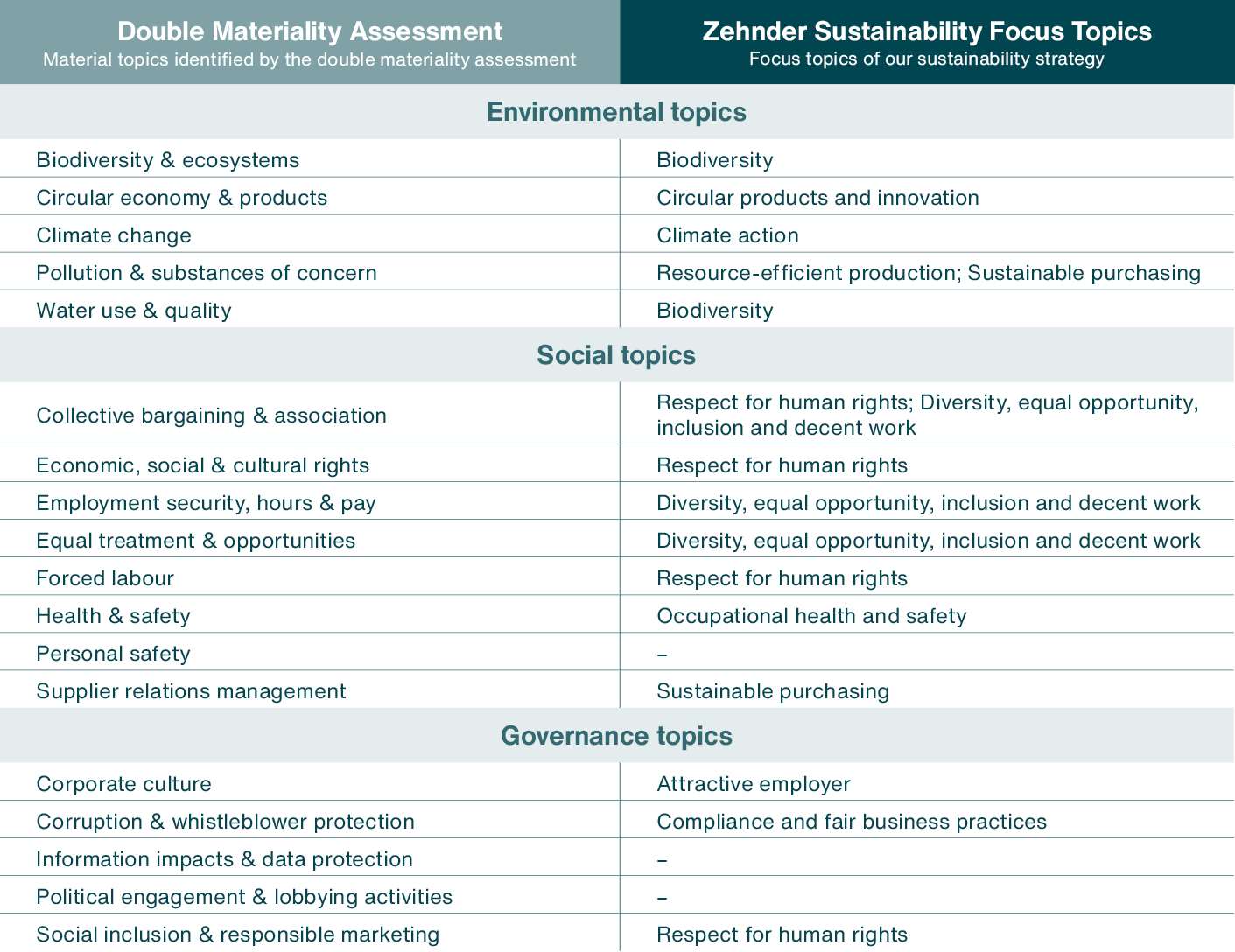

The assessment generally affirmed our understanding of the prevailing material topics. Based on the results of the survey, we identified the most significant material topics for each area of Environment, Social and Governance. Those have been integrated in our sustainability strategy and are elaborated upon in this report. Three topics from the double materiality assessment are not addressed here, as they are already managed through existing processes within Zehnder, outside the realm of the sustainability strategy.

1 The European Sustainability Reporting Standards (ESRS) are standards that define the rules of the Corporate Sustainability Reporting Directive (CSRD): ESRS 1: General requirements - Appendix A.

Stakeholder analysis

For Zehnder Group, the stakeholder analysis represents an essential component of our Sustainability Report. It enables us to better understand the interests and needs of our relevant stakeholder groups. We define stakeholders as individuals and organisations that have financial, legal, ethical or environmental expectations of Zehnder Group. Zehnder Group aims to create transparency regarding the Group’s commitment to sustainable development and to maintaining an open and respectful dialogue with its stakeholders. Through routine, transparent communication, we seek to further strengthen trust in our company and to maintain or establish long-term relationships with our stakeholders.

Communication with stakeholder groups

In 2023, we focused our stakeholder communication on employees, customers, suppliers, investors, financial analysts, rating agencies and non-governmental organisations in particular. Overall, Zehnder uses a variety of tools and channels to communicate with the above mentioned stakeholder groups:

- Through our publications such as the Annual Report and Sustainability Report as well as ad hoc and media releases, we keep shareholders and other stakeholders updated regarding key figures, the status of our sustainability activities and hot-button topics at Zehnder Group.

- Concerning investors, we conduct an annual presentation for analysts and the media. We also participate in various investor and analyst roadshows and conferences as well as host investor days.

- Meetings on corporate governance involve discussions with investors and proxy advisors and are attended by the Chair of the Board of Directors.

- To better understand stakeholder expectations for our sustainability journey, we conducted a double materiality assessment with a range of stakeholders.

- We regularly share information with our customers during trade fairs, customer visits and training courses.

- We are in frequent contact with sustainability rating agencies.

- Through our active engagement in a number of areas, we are in close touch with subject matter experts and specialists of various organisations, like the UNGC and similar.

- Performing our supplier screening, assessments and audits, we work closely with our high-risk suppliers when it comes to sustainability.